Published on

17 June 2026

Most KYC teams believe reviewing everything means safer compliance, but calendar-based models dilute analyst attention and leave high-risk cases under-resourced. Discover why risk-triggered reviews outperform fixed cycles, and what good looks like in practice.

By Vimalan Pillai, Assistant Vice President, Delta Capita

The file had been sitting in my QC queue for two days. Forty-three pages. Clean history. No change in ownership. No new jurisdictions. No red flags. A low-risk retail client on a calendar cycle, reviewed because it was their turn. I spent an hour on it. So did the analyst before me. So did the relationship manager who chased the document refresh. Somewhere else in the queue, an Enhanced Due Diligence (EDD) case with a new beneficial owner in a sanctioned jurisdiction was waiting.

I’ve spent three and a half years at Delta Capita in a quality control role, reviewing case after case flagged for periodic review. After a while, you start to notice a pattern: a lot of what lands in the pipeline didn’t need to be there.

Low-risk retail clients with no change in circumstance. Dormant accounts that haven’t moved in 18 months. Standard onboardings held up because they fell into a blanket review cycle rather than anything that warranted scrutiny. As a QC analyst, your job is to catch errors and assess whether the right decisions were made. But when the volume is inflated with unnecessary reviews, you spend just as much time questioning ‘why was this reviewed at all?’ as you do checking whether it was done correctly.

That’s the core problem with calendar-based, ‘review everything’ KYC models: they feel safe. But they’re not actually risk-driven.

Hard Truth #1: Reviewing Everything Doesn’t Make You Safer, It Makes You Slower

There’s a logic to it. If you review everything, you can’t be accused of missing something. Regulators want to see that you know your client, so surely more reviews mean more knowing?

Not really. What it creates is noise. When analysts are processing a high volume of low-risk reviews on rotation, attention gets diluted. The genuinely high-risk cases, the ones showing behavioural changes, new beneficial owners, or links to sanctioned jurisdictions, get the same queue treatment as the client who’s had the same two direct debits for five years. That’s not risk management. That’s throughput management dressed up as compliance.

From a QC perspective, I’ve seen this play out in quality scores too. Error rates tend to spike not because analysts don’t know what they’re doing, but because fatigue and volume pressure on low-value work leads to missed flags on the cases that actually matter.

Hard Truth #2: Risk-Based Doesn't Mean Light-Touch; It Means Calibrated

The Financial Action Task Force (FATF) Recommendations and the Financial Conduct Authority's (FCA) own guidance are clear: a risk-based approach means your controls should be proportionate to the risk identified. It doesn’t mean doing less. It means doing the right things, for the right reasons, at the right time.

A genuinely risk-triggered review model asks a better question than ‘when did we last review this client?’ It asks: has anything changed that affects this client’s risk profile?

The Five Triggers That Should Drive a Periodic Review

- A change in UBO or control structure

- A new high-risk jurisdiction in the client’s transaction profile

- A spike in activity inconsistent with their stated business

- A PEP connection emerging post-onboarding

- A negative news hit or sanctions list match

If none of those triggers are present, a low-risk client with a clean history doesn’t need to be pulled into a full periodic review on a fixed cycle. They need monitoring, and if the monitoring is working, it will surface the trigger when it matters.

Hard Truth #3: Volume Pressure on Low-Risk Work Degrades Quality on High-Risk Cases

The most common failure mode I’ve reviewed isn’t an analyst making a bad risk decision. It’s the system setting analysts up to make decisions that don’t need to be made at all. When your workload is dominated by routine, low-risk reviews, a few things happen consistently:

- Outreach fatigue sets in. Clients are contacted for document refreshes when nothing has changed, damaging the relationship and creating friction for no risk benefit.

- Onboarding slows down. New clients with straightforward profiles get queued behind a backlog of unnecessary periodic reviews.

- High-risk work gets under-resourced. When capacity is limited, volume affects quality.

I’ve quality-checked files where an analyst clearly rushed an EDD case, not because they didn’t understand it, but because they had 40 other cases in the queue, most of which were standard low-risk renewals. That’s a systemic problem, not an individual one.

Hard Truth #4: Outreach Fatigue Isn’t Just a Client Problem, It’s a Capacity Problem

In Blog 2 of this series, we explored how poor client outreach is where KYC inefficiency first becomes visible to your clients. Calendar-driven reviews compound this. When low-risk clients are repeatedly contacted for documentation that hasn’t changed, they disengage. Relationship managers get frustrated. And the outreach capacity that should be reserved for genuinely complex or time-sensitive cases gets absorbed by unnecessary touchpoints.

The result is that the clients who most need clear, prompt, well-structured outreach, those going through EDD or event-driven reviews, often receive the least attention. Not because the team doesn’t care, but because the workload model doesn’t allow for it.

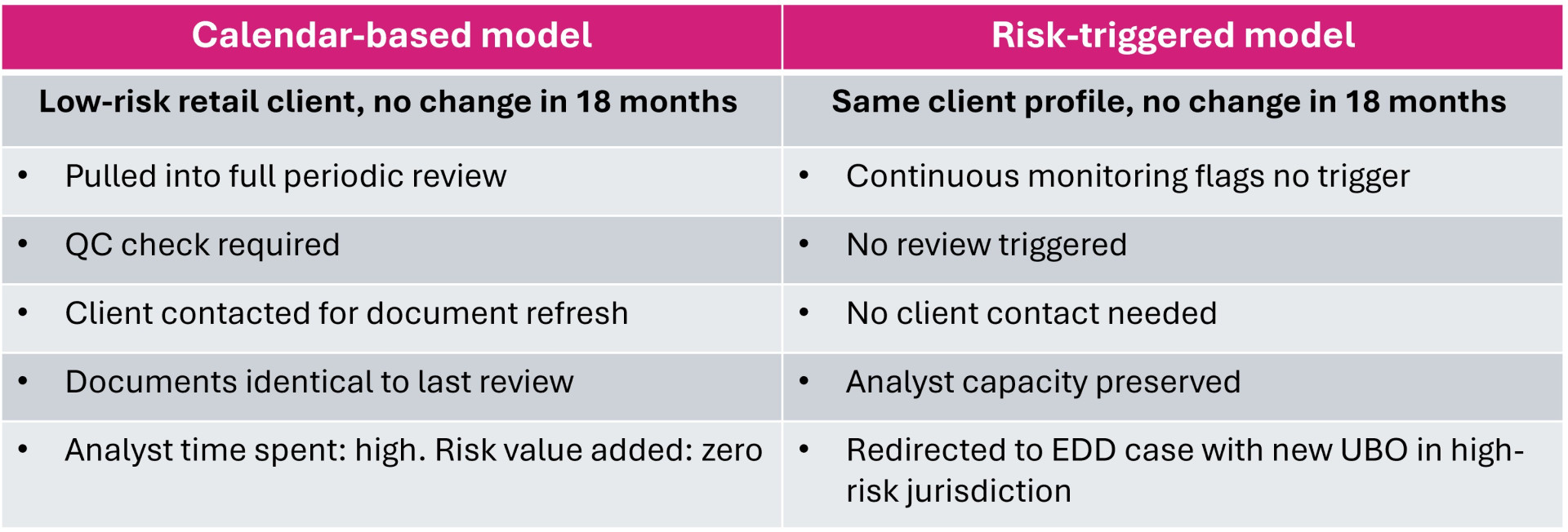

What Good Looks Like: A Side-by-Side

The shift from a calendar-based model to a risk-triggered one changes what analysts spend their time on. Here’s a concrete illustration:

This isn’t a theoretical improvement. The banks getting this right have moved away from fixed review cycles for low-risk segments and toward event-driven, risk-triggered models. Reviews happen when something changes, not just when the calendar says so. Monitoring does the heavy lifting in between, and analysts are deployed where human judgement adds value.

Key Takeaways

- Most KYC inefficiency isn’t caused by bad analysts; it’s caused by badly designed review triggers.

- Calendar-based models dilute analyst attention and offer false assurance of compliance rigour.

- FATF and FCA guidance explicitly supports proportionate, event-driven approaches – doing less isn’t the risk.

- Risk-triggered models improve both compliance quality and analyst capacity, because the cases coming through for review are the ones that warrant it.

- The right question isn’t ‘when did we last review this client?’, it’s ‘has anything changed that affects their risk profile?’

How Delta Capita Can Help

Delta Capita helps financial institutions move from calendar-driven review models to genuinely risk-calibrated KYC, across the full client lifecycle, from operating model design through to technology-enabled delivery and managed services.

Delta Capita also provides seasoned KYC analysts, QA reviewers, and SMEs with deep experience across onboarding, remediation, event-driven reviews, and policy design, helping firms simplify KYC execution while maintaining rigorous risk standards.

Ready to move from calendar-driven reviews to risk-calibrated KYC? Let’s talk.